Price Is Not Created at the End: Why Competitiveness Is Shaped Upstream

Most post-award debriefs have a familiar rhythm: teams gather after a loss, customer feedback is reviewed, the scoring is dissected, and the price comparison gets pulled up. Eventually, someone says some version of the same thing:

“We lost on price.”

That may be true at the surface level. But, it is usually not the full explanation.

In federal contracting, companies invest enormous time, money, and executive attention into capture and proposal efforts. They build qualified teams, develop detailed technical solutions, sharpen win themes, and run disciplined color team reviews. Yet many still lose without a clear understanding of why. The explanation defaults to broad labels: price, technical, incumbent advantage, past performance or customer preference.

Those labels may describe the outcome, but they do not diagnose the underlying problems. This is especially true with price.

When teams say, “We lost on price,” they may mean the final proposed price was higher than the winner’s. They may mean the customer placed less value on their technical premium than expected. They may mean the bid was penalized through cost realism, most probable cost adjustments, staffing concerns, or another evaluation mechanism. Or, they may mean the competitor had a fundamentally different labor mix, team structure, or indirect cost position.

Those are not the same problem. Treating all of these as “we lost on price” guarantees that the real lesson will be missed.

The better question is, “What decisions caused our price to become what it was?”

Price Is an Output, Not an Isolated Decision

The most important thing to understand about price is that it is usually not created when the pricing team builds the final cost volume. By then, the largest economic decisions have typically been made, and much of the price has already been shaped.

The customer has defined the scope. The contract type has been selected or heavily influenced. The CLIN structure has been established. Labor categories and minimum qualifications may already be defined. Section L has told offerors what to submit. Section M has told evaluators what to value. Sample tasks, transition requirements, key personnel rules, small business expectations, and price evaluation mechanics may already be in place.

Inside the company, the team has likely already made major decisions about teaming, workshare, staffing, solution design, transition approach, technical narrative, and delivery model. Each of these decisions narrows the range of prices a bid can credibly support.

By the time the pricing team builds the pricing model, it is operating inside a box constructed much earlier. Pricing can still sharpen the bid. It can test assumptions, pressure subcontractor inputs, refine escalation, evaluate fee, and identify inconsistencies. Those actions matter.

But, they are usually optimizations inside the box, not a redefinition of the box itself.

That is why late-stage pricing efforts often feel limited. Teams cut fee, revisit escalation, squeeze labor assumptions, or put the screws to teammates for better rates. Sometimes those changes help. But if the procurement structure favors a different delivery model, a different staffing strategy, or a different cost architecture, late-stage pricing actions are working around the edges of a much larger issue.

The price model is the output. The upstream decisions are the input.

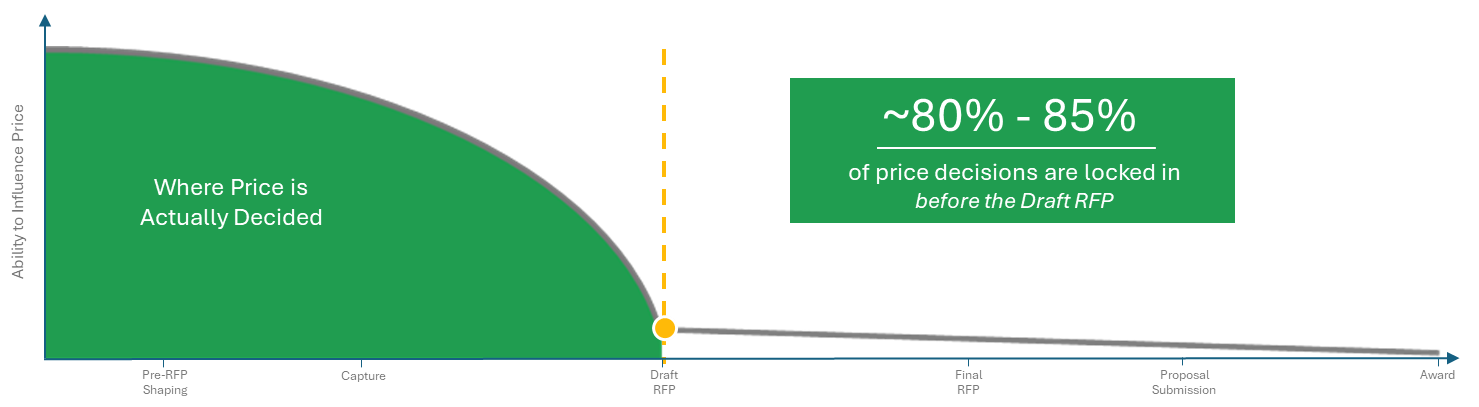

The Box Is Built Before the Draft RFP

Capture teams often say they need to “start early.” That is true, but the phrase can become too generic to be useful.

Starting early does not simply mean beginning the proposal before the final RFP is released. It means influencing the economics that shape the opportunity before the rules of the game are locked in.

Every procurement creates a box. The scope of work, contract type, CLIN structure, labor categories, qualification requirements, price schedule, Section L instructions, Section M evaluation criteria, and realism provisions define how bidders will compete.

We estimate that 80–85% of the meaningful decisions that bound price are typically locked in by the time the Draft RFP releases. There may still be room to influence language between Draft and Final RFP, but by that point, companies are usually influencing clarifications, refinements, and evaluation details rather than the major economic architecture of the procurement.

Pre-Draft RFP decisions are not just procurement mechanics. They are economic design choices.

They establish who can be competitive, which delivery models are credible, which competitors are advantaged, which bidders can price aggressively, and which solutions will look risky or expensive.

When a team loses by 1%, 2%, or 5%, the instinct is to look at those late-stage levers and ask what could have been sharpened. Sometimes the answer is real. More often, the answer is that the box was already too small to win inside, no matter how hard pricing worked at the end.

This is why many larger contractors are moving pricing, PTW, and strategic pricing personnel earlier in the business development and capture process. In some organizations, those roles are being redefined entirely — less as back-end pricing support and more as deal architects, competitive strategists, or pursuit economics advisors. The titles vary, but the logic is the same: if the economics of the bid are shaped upstream, then the people who understand those economics need to be involved upstream.

That does not mean pricing owns capture. It means capture, BD, pricing, contracts, technical leadership, and proposal teams need a shared view of how the opportunity should be structured before the RFP arrives.

That is where a desired-state playbook becomes useful.

Create a Desired-State Playbook

Shaping RFPs is obviously not new, and it is hard work. But if price is shaped upstream, then competitiveness has to be managed upstream as well.

Teams should translate their competitive strengths into a preferred solicitation structure — what we call the “Desired-State Playbook”.

A desired-state playbook is a written articulation of what an RFP should look like for your company to be advantaged on the pursuit. It is built before the Draft RFP exists. It is developed jointly by capture, BD, proposal, technical, pricing, and contracts. And it answers one specific question:

If we could shape this procurement, what structure would we shape it into?

That is different from the question most capture teams ask. Most teams ask: What do we know about how the customer is going to structure this? The desired-state question is more aggressive: What structure advantages us most, and how do we help move the customer toward it?

The answer is rarely a single decision. It is usually a set of structural choices that compound. Evaluation criteria weighting. Section L page allocations. Labor category definitions. Sample task structure. Past performance relevance criteria. Price realism treatment. Small business workshare requirements. The contract type.

Each of these is an economic design choice that establishes who can compete and who cannot. Most companies have not translated their competitive strengths into preferred positions on these choices.

What Goes into the Playbook

Think of the desired-state playbook as drawing up your best plays in Xs and Os before the game starts. The playbook identifies which plays create favorable matchups and which plays to run when you get certain looks.

It is not enough to know that your company has strong technical depth, a credible delivery model, customer intimacy, price flexibility, or strong past performance. The real work is translating those advantages into the procurement structure itself.

A useful playbook covers three areas:

Where your strengths map to evaluation structures.

If your advantage is technical depth, what evaluation structure rewards it? More technical page count, more weight on the management approach, more emphasis on key personnel, more detailed sample tasks, a stronger evaluation of risk?

If your advantage is price flexibility, what structure rewards it? Looser labor category definitions, minimized pricing submission requirements, a pricing structure that rewards efficiency?

If your advantage is delivery credibility, what structure rewards it? Price realism, a priced basis of estimate, transition evaluation, an explicit connection between staffing and technical approach?

Most companies know their strengths. Fewer have translated them into preferred Section L and M positions.

Trigger points and contingencies.

Shaping is a probability exercise, not a certainty exercise. The playbook should describe what happens if the customer makes certain choices.

What do we want if the customer includes price realism? What do we want if the customer uses a sample task? What do we want if the customer requires a specific small business workshare? What do we want if the customer defines labor categories tightly?

Each contingency triggers a different bid posture. The playbook should anticipate those scenarios before the RFP arrives.

Specific shaping actions.

The playbook should be operational.

What conversations should be had with the customer, by whom, and when? What white papers should be drafted to introduce specific concepts? What demonstrations or briefings could move the customer toward the desired structure? What industry days or RFI responses should be used to surface particular ideas.

The shaping work is not abstract. It is a campaign of specific actions over specific time periods, and the playbook tracks them.

The goal is to have your best plays drawn out before the structure is locked in. By the time the RFP arrives, the team should already know what it wanted, what it achieved, where it remains exposed, and how the bid posture must adjust.

Why This Is the Work BD and Capture Should Be Doing Now

This work matters more as the Government moves toward fixed-price, outcome-based contracting.

Under cost-type or labor-hour structures, the range of viable pricing outcomes is often more constrained. Fixed price changes that dynamic. It gives bidders more room to structure the work differently — through labor mix, staffing flexibility, automation, reach-back, shared services, delivery centers, teammate strategy, or execution risk.

As a result, the upstream pricing factors matter more. The goal is not simply to react to the RFP once it is released. The goal is to shape the economic conditions under which the competition will be fought.

The desired-state playbook makes that work deliberate. It forces the team to ask, before the Draft RFP: What pricing factors matter most? Which ones can we influence? Which ones advantage us? Which ones advantage the competition?

In a market moving toward fixed-price, outcome-based contracting, the companies that understand the economics earlier will be better positioned to shape the competition before the price is ever built.

The Bottom Line

Price is not created at the end of the process. It is shaped upstream. By the time the final price is calculated, many of the biggest drivers of competitiveness have already been established: the solicitation structure, contract type, evaluation model, teaming strategy, labor mix, technical approach, and risk narrative.

Pricing still matters. But pricing works inside the economic structure the pursuit has created.

For BD, capture, and proposal teams, the implication is clear: you may not own the final price, but you absolutely shape the economics that make the price credible. The companies that understand this will stop treating price as a late-stage adjustment. They will start treating competitiveness as an upstream design problem. And in a market where customers are increasingly focused on outcomes, affordability, and execution risk, that distinction may be the difference between a bid that is merely compliant and a bid that is built to win.

At BlackFlag Advisors, we help teams understand the upstream Price-to-Win decisions that shape competitiveness long before final pricing begins. By integrating PTW and competitive intelligence, we help contractors identify the economic levers that determine whether a bid is truly positioned to win.

Need help shaping the economics of your next pursuit before the RFP locks them in? Let’s talk.